Avoid These 12 Common Investing Mistakes to Grow Richer

The small investing mistakes that delay financial independence and the simple systems that fix them permanently.

Last month, I realized I hadn’t turned on dividend reinvestment for a major ETF. What an unforced error! Especially for someone like me who does this stuff every day.

I started visualizing a week of my future freedom vanishing because I wasn’t paying attention. Complexity catches up to us all at one point or another.

That inspired this review. Every dollar you lose to these mistakes is another day or week you are forced to work for others rather than for yourself. Another day of being tethered to a desk instead of your dreams.

The good news is that plugging these leaks is one of the easiest ways to build wealth and spend less time thinking about your money.

That’s because these create a hidden Complexity Tax on your life. One that you can quickly fix it with simple systems.

“It is remarkable how much long-term advantage people like us have gotten by trying to be consistently not stupid, instead of trying to be very intelligent.” - Charlie Munger.

The Behavior Mistakes That Eat Your Returns

1. Trying to time the market

Maybe you pause contributions because “things look shaky.” You move part of your portfolio into cash to keep some “dry powder.”

Unfortunately, markets tend to recover before we feel safe.

Missing the best 10-20 trading days destroys long-term returns. From 2002 to 2021, staying fully invested in the S&P 500 returned 9.5% annually. Missing just the 10 best days dropped that to 5.3%. Missing the 20 best days? 2.6%.1

This mistake is so common because it feels responsible. Yet, the compounding damage comes from missing just a handful of strong days, plus the psychological hurdle of reinvesting once prices rise. Timing the exit is hard. Timing the re-entry is even harder.

A better rule is: automate your investing on a schedule, stay the course, and let time do the heavy lifting.

2. Changing your allocation during stress

This one is a cousin of market timing, but it deserves its own category because it tends to be permanent.

You start with a 90/10 portfolio of stocks and bonds. Then a real drawdown hits. The market falls 20 or 30 percent, and your account balance is significantly down. The economy is in the dumps.

So you reduce risk. You sell into safer assets right after the drop.

On paper, this feels like prudence with a weak economy. In practice, it locks in losses and reduces your participation in the recovery.

It also creates a new problem: when do you raise risk again? The same fear that pushed you to de-risk will keep you from reentering the market.

This bad timing costs investors about one-fifth of their returns or (-1.7%) according to Morningstar.2

Instead, choose today a portfolio that you can actually stick with. A slightly more conservative allocation that you can hold for 20 years is better than an aggressive allocation you abandon.

3. Letting cash build up unintentionally

Cash drag is one of the most underappreciated tactical mistakes, especially for high earners.

It shows up as:

bonuses sitting in checking

“temporary” cash parking that lingers indefinitely

transfers that land in a brokerage settlement fund and never get invested

indecision about where to invest (analysis paralysis)

It costs you in terms of immediate returns and all the compounding future returns you’ll miss.

Automatic contributions and investing solve this for you. Make sure your investing platform allows it and go set it up today.

4. Not increasing investments as income rises

Many investors set their investments and retirement contributions once and never touch them again.

Meanwhile, income grows, which usually leads to lifestyle inflation.

It doesn’t even feel like a mistake because you’re still investing. You’re still doing more than most people. But a savings rate that slides from 25 percent to 15 percent is a major shift in your financial trajectory. It pushes financial independence and your goals further into the future.

The easiest fix is automatic escalation in your 401(k). Raise contributions by 1 percent each year, or set a rule that every raise or bonus triggers an increase. It is by far the easiest way to become a multi-millionaire.

Tax Mistakes That Suck Your Money

The biggest tax errors are rarely about complex loopholes.

The errors come from misunderstanding the basics, missing simple settings, or not using the tools you already have.

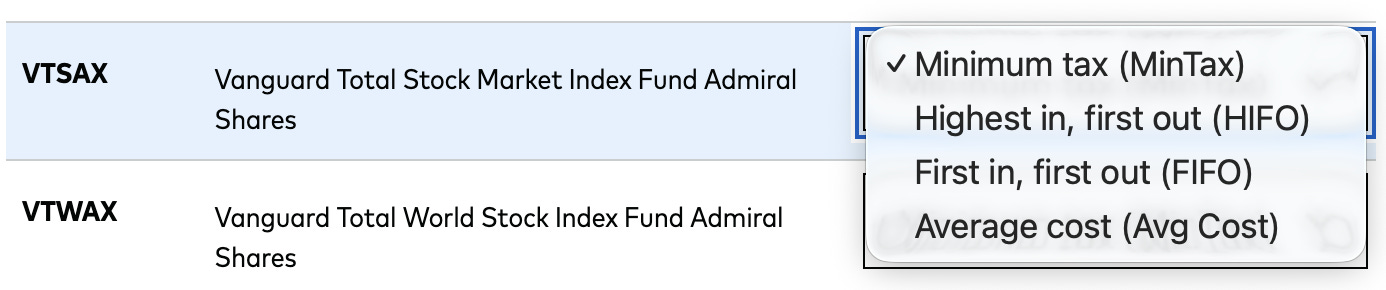

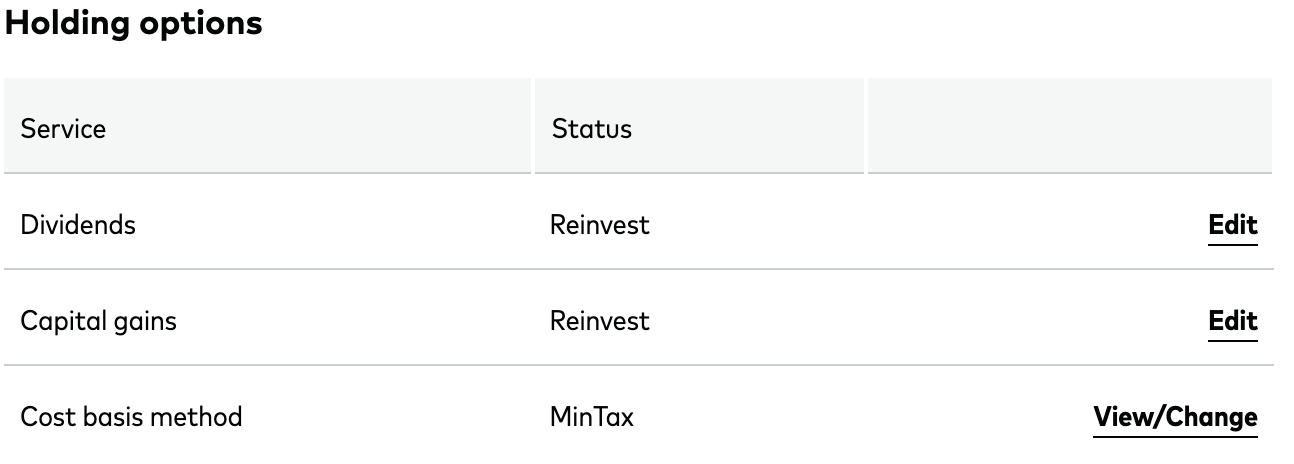

5. Not updating your cost basis method

This one matters most in taxable brokerage accounts and especially with mutual funds.

Many brokerages default to a cost-basis method such as FIFO (first-in, first-out) or average cost. Those defaults can create unnecessary taxable gains when you sell, because they don’t let you choose the most tax-efficient shares.

Instead, use Minimum Tax (MinTax) or specific lot identification (SpecID). These allow you to often reduce your capital gains by selling the highest-cost shares first. That can mean thousands saved on a single sale and much more over a lifetime.

Go to your brokerage settings and update them like this example from Vanguard:

6. Not harvesting tax losses

Market losses create opportunity in taxable accounts. When assets drop below your purchase price, you can harvest the loss, reduce current taxes, and reinvest to stay in the market.

Tax-loss harvesting lets you deduct up to $3,000 per year from ordinary income. Unused losses carry forward indefinitely. Over 30 years, consistent harvesting can save $40,000+ in taxes at higher brackets.3

Tax loss harvesting adds a little record-keeping that may feel like extra work, but think of it as a side hustle. How much time would you invest in a side hustle for $40,000? And often you can do a tax-loss harvest one time and carry forward the $3,000 per year for a decade or more.

7. Poor asset location

Most people understand asset allocation: how much they hold in stocks, bonds, cash, and other assets.

Fewer people think about asset location, which is where you hold each asset within taxable, tax-deferred, or tax-free accounts.

The placement matters because different assets generate different kinds of taxable income. Putting tax-inefficient assets in taxable accounts can create ongoing tax drag. Putting tax-efficient assets in IRAs can waste valuable space.

It’s less complicated than it sounds. The general idea is:

keep tax-inefficient income-producing assets in tax-advantaged accounts when possible (e.g., bonds, REITs, high dividend stocks, actively managed funds)

keep tax-efficient stock exposure in taxable accounts when it fits your plan (e.g, stock index funds, municipal bond funds, stocks you hold for the long-term)

Set it up once and benefit for decades.

The Fee And Structural Mistakes That Are Relentless

8. Paying high expense ratios without realizing it

Fees are one of the few guaranteed negatives in investing. And because they’re expressed as small percentages, they’re easy to dismiss.

But a 1% fee versus a 0.1% percent fee is not the same. That difference could cost you hundreds of thousands of dollars over your lifetime.

Make sure you know your all-in costs and use low-cost index funds as much as possible. As a general rule, I consider anything over 0.25% to be a high fee.

9. Leaving old 401(k)s unmanaged

Old employer 401(k) or 403(b) plans often sit untouched and forgotten for years. That can mean:

higher fees than your current options

mediocre fund lineups

no rebalancing

forgotten allocation drift across your household portfolio

Even if you leave an old 401(k) where it is, it should still be part of your total portfolio plan. In many cases, consolidating accounts or rolling into a better plan reduces complexity and saves fees.

Execution Errors That Prevent Compounding

10. Forgetting to turn on dividend reinvestment

Dividends are a major driver of long-term equity returns. If dividends aren’t reinvested, they become idle cash and the compounding engine loses power.

From 1980 to 2019, 75% of S&P 500 returns came from reinvesting dividends!4

This one is painful because it’s purely about one specific detail. You can do everything right and still miss huge gains if you never toggle that setting.

Check your account settings. Make sure dividends and capital gains distributions are reinvested in all your accounts, if that aligns with your plan.5

11. Failing to rebalance systematically

Without rebalancing, portfolios drift away from your plan.

If stocks rally for years, your 70/30 can easily become 85/15 or 90/10. That means you’re taking more risk than you intended, often right before a drawdown reminds you what risk actually feels like.

Rebalancing is not about predicting markets. It’s about maintaining your chosen risk level and forcing discipline: trimming what has grown and adding to what has lagged.

Pick a rule you can follow and do it once or twice per year. It could be calendar-based, threshold-based, or a combination.

12. Creating too many small positions

This is a modern problem. With zero-commission trading and endless content, it’s easy to accumulate a messy portfolio. Especially with new platforms popping up every day and offering incentives to set up an account.

Too many positions creates:

rebalancing headaches

tax complexity

unclear exposure and allocation

more opportunities to make mistakes

Complexity is not sophistication. It creates more opportunities for problems and more headaches to manage for no added benefit.

Create Systems To Remove The Complexity Tax

Every mistake in this post has a common root: complexity. Complexity is a tax that sucks time, money, and energy. It leads to worse decisions and mental load.

The antidote is more systems.

automatic contributions

automatic investing

a fixed allocation you can hold through volatility

a simple fund lineup

cost basis settings and tax rules handled upfront

scheduled rebalancing

You’ll create a simpler portfolio that is easier to manage, easier to rebalance, and stick with.

You’ll build the wealth so you can go create the life your wealth is meant to pay for.

Which of these 12 are you currently guilty of? Leave a comment.

Disclaimer: This article is for general education only. It isn’t personal financial advice. I don’t know your whole situation, goals, or risk tolerance, and nothing here should guide your decisions on its own. Do your own research or speak with a professional before acting on any investment ideas.

https://fmpwa.com/the-cost-of-missing-the-10-best-days-in-the-stock-market/

https://www.morningstar.com/funds/bad-timing-cost-investors-one-fifth-their-funds-returns

Assumes harvesting $3,000 per year for 30 years at 45% combined state and federal tax bracket.

https://gfmasset.com/2019/07/75-of-sp-500-returns-come-froa single,m-dividends-1980-2019/

There are times, when you don’t necessarily want to reinvest dividends, most commonly when retired and planning to use them to fund your expenses.