The $400,000 Mortgage Mistake Most People Make

Pay off your mortgage or invest? A wealth building framework that gives you more options.

My neighbor Alan just got back from a round-the-world trip with a family of four.

A year ago, Alan quits his job, and his whole family jumps on a plane to Korea, where they are from.

His two sons immediately enroll in school there. They spend 6 months making friends and getting to know their aunts and uncles. They explore all over the country. His sons get comfortable speaking Korean fluently for the first time.

When the semester ends, they start worldschooling. Six more months of learning and traveling with stops in Cambodia and the Great Barrier Reef before finishing with a month in the French countryside. They are now home and reenergized for life.

Wealth = Choice

Stories like Alan’s are achievable for people who understand how to use their wealth to create more choice. Choice in how to spend your time, location, and career. And you can do it on a middle-class lifestyle, like Alan.

And there’s one major mistake people make that takes away their future choices and costs them hundreds of thousands of dollars.

They pay off their mortgage too early.

Managing the biggest financial commitment: a mortgage

I’m going to take a deep dive on this question of “Should I pay off my mortgage or invest?” in the context of a framework that’s designed to make you wealthier and to give you more choice.

Although I’m discussing mortgages, the principles I share in this article apply to all wealth decisions. Renters and people with paid-off mortgages will still take away a framework for prioritizing how they build wealth and create choice.

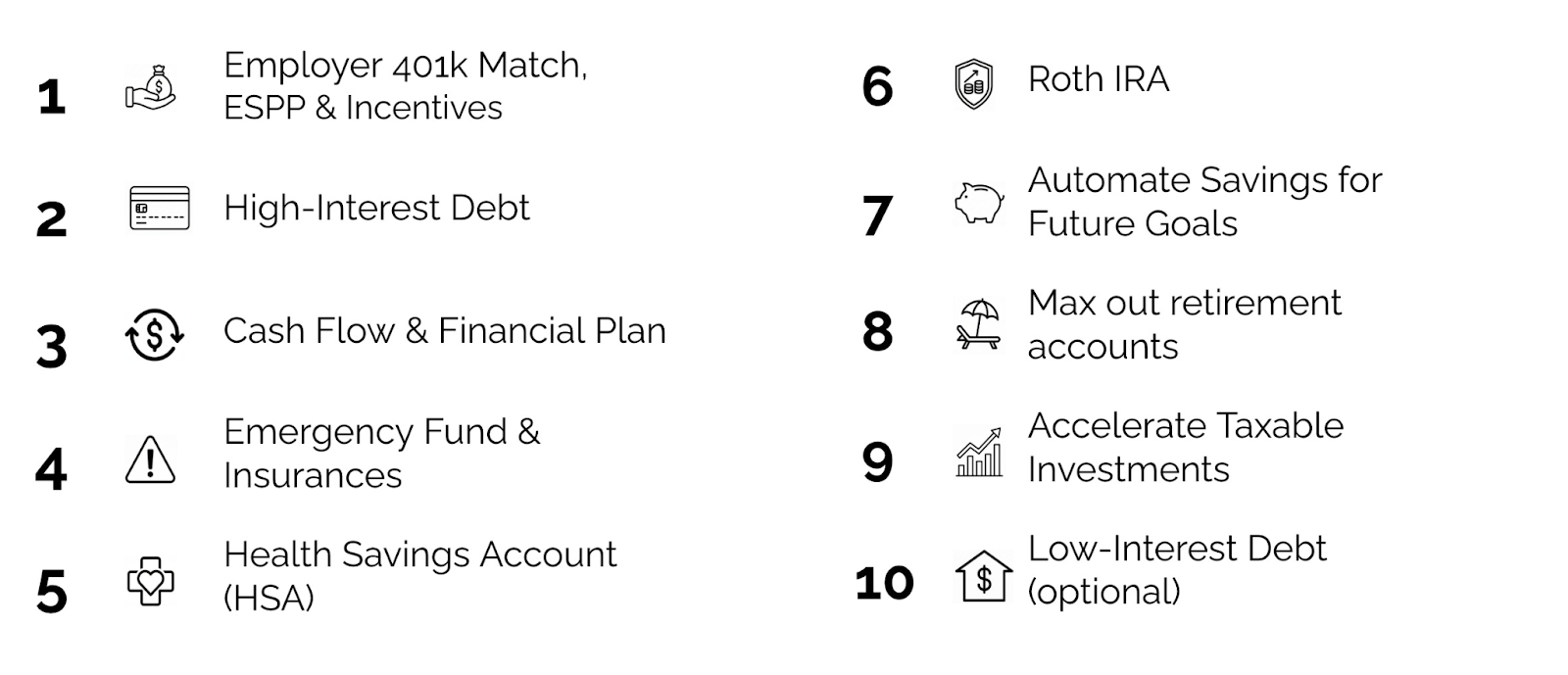

The 10 Steps to Life Changing Wealth

There is a clear, fastest, and smartest route to building life changing wealth. The kind of wealth that Alan has.

I’ve shared it in my 10 Step framework. You can read the full overview here.

Paying off low-interest debt is the final optional step. That’s by design.

The goal is to build wealth to have more control over your work and life along the way.

The goal isn’t to defer your life into the distant future. Or to prioritize removing debt as quickly as possible. Those are decisions driven by fear rather than opportunity.

By doing steps 1-9 first, you’ll move faster toward a future full of choices where you can travel, make career pivots, and live differently.

Let’s go through them now.

Start by checking your financial foundation: Steps 1-4

If you are considering paying off your vs. investing more, first check:

Are you getting your full employer match? [Step 1]

Do you have high-interest debt (eg, credit cards)? [Step 2]

Are you tracking your spending and know what’s coming in and out? [Step 3]

Do you have an emergency fund and basic insurances? [Step 4]

Take any steps you’re missing. Then move on.

Then move to funding your future next: Steps 5-8

If you have extra funds, you also need to ensure your savings and retirement are rock-solid. Why?

A funded retirement gives you control and leverage immediately.

Fully funding your retirement is as much about now as it is about later. The more future-you is funded, the more present-you can take career risks and design work that fits your life.

Retirement gives you access to the most powerful wealth-building strategies.

Maximizing your investment in your retirement accounts has two big wealth-building advantages:

These accounts give you significant tax savings. With smart tax planning, you can effectively earn 15-25% more on your investments through lower taxes.

The 2025 tax law increased the SALT deduction cap, meaning more homeowners can now deduct mortgage interest. (Applies to some cases, particularly in high tax states.)

What to do last: Invest before Paying The Mortgage.

Once you have completed Step 8, you’ll have a secure foundation and retirement.

At this point, investing extra funds still gives you more wealth and more options than paying your mortgage. There are several reasons.

1. Investments create income and choices now

This gets at the heart of thinking about giving yourself choices in how you live your life.

Invested assets don’t just grow in the background waiting for old age. They create options you can exercise immediately and at any time in the future.

A paid-off house only helps after it is paid off in 30 years.

An investment portfolio can throw off dividends, interest, or gains you can use to:

Take a sabbatical

Try a career change

Fund time with your kids

How could you use investment income to improve your life?

2. You’ll almost always be richer by investing

If your expected investment return is higher than your mortgage rate, you build more wealth investing. It’s as simple as that.

Let’s say you have an extra $750 to invest each month and you are debating between investing it in the stock market vs. paying down the mortgage. We’ll assume you have a $500,000 mortgage at a 4.5% rate and expect an 8% return on the stock market.

How would your wealth grow in either scenario?

After 30 years, you have a paid-off house in both scenarios. But by investing, you would have made $410,000 more and had more choices the entire time.1

3. Real Estate doesn’t always go up.

Investing your money in stocks and bond funds keeps your assets flexible while you diversify your investments instead of concentrating them on real estate.

You still build home equity through your regular mortgage payments, while building more accessible wealth in a diversified investment portfolio.

Recent years have shown that the belief “real estate always goes up” is simply not true.

Housing prices are down year over year in many desirable metro areas like Austin (-7.3%), San Diego (-6.7%), San Jose (-5.5%), Minneapolis (-4.9%), and Washington DC (-4.8%).2

Remember that stocks have outperformed real estate on average.

4. Liquidity gives you contingencies when life throws a curve ball

Jobs change. Health changes. Families change.

Every dollar you send to your mortgage is a dollar you can’t touch.

If you get sick or lose your job, having cash and liquid investments to support yourself is incredibly valuable. You can adapt without scrambling for a HELOC or selling your home at the wrong time.

You can make other choices in life knowing you are prepared if things go wrong.

5. You can always pay off the mortgage later

Once you send extra money to your lender, you can’t easily get it back. (You generally have to pay for taking out a refi or a HELOC.)

But if you invest instead, you can still pay off the house at any time in the future, including by using the money you earn from those investments.

If you wake up at 55 and want the house paid off, you can write a check. But if you’ve previously paid off your house and then need cash, you’re stuck.

Keep the mortgage

Investing and wealth-building are primarily a game of managing our behavior and feelings toward money.

Some people will tell you it’s OK to pay off your mortgage if it makes you feel better and helps you sleep at night.

But it comes at a huge cost and hidden risks.

I know that debt can feel scary. But so can investing your money for the first time.

If you can learn to examine those parts of your emotions and stil to make money decisions based on a thoughtful plan for your life, you will reach your goals much faster.

—

Please share in the comments: What choices do you want your investments to buy you in the next 5 - 10 years?

A few other what-if analyses are also interesting. What if your mortgage and investment return are the same? You still would have more wealth by investing through the entire 30 year period if you use the month to invest rather than pay down the mortgage. That is, up until the very last day of the 30 years, when they would reach wealth parity.

And what if your mortgage rate is higher than investment return? Say your mortgage rate was 6% and investment returns were pretty low at 4%? Well, you would still be better off investing for the first 26 years! It would only be in the last 4 years when the results flip and paying down the mortgage has a higher expected wealthin, D.C.curveball.

https://www.realtor.com/news/trends/home-prices-falling-fastest-december-2025/?utm_source=chatgpt.coare buildingstillofareto move forward wisely despite ourthought-outm

A clear reminder that strategically investing before aggressively paying down a low-rate mortgage can maximize wealth and create real-time lifestyle flexibility

James, excellent post, as usual. I decided to sell my home, grab the equity, invest and now I’m renting. My house sold at around 1 million with a small mortgage. Now I have no worries or sleepless nights about spending money on lawn care, landscaping, home repairs, etc. I can now go on vacation and close the apartment door and not care one bit about storms, break ins, etc. Also, when I pass my kids won;’t have the hassle of selling the house. Time will tell if the investment piece works out but I believe the market should out perform the value of the house.