How to avoid a disaster investing in rental property. And what I did instead.

The math of a bullet dodged: Real estate investing vs. the stock market

In 2022, I dodged a bullet. I was closing on a property that I planned to Airbnb. I’d spent weeks researching markets, subscribing to Airbnb data services, and running projections. I found a property in a mountain town and felt good about the numbers.

At the 11th hour, thankfully, I phoned a friend.

He is an experienced Airbnb investor. He looked at my spreadsheet and asked where I’d accounted for cleaning costs between guests. It’s not that I’d forgotten them. I’d accounted for them differently than Airbnb does.

That accounting detail turned my projected profit into a -$10k yearly loss.

I resisted that realization at first. I was excited about a new investment and owning more property. I tried to rationalize that the operating loss was ok. I told myself I locked in a great interest rate while rates were rising. I told myself the property is probably going to appreciate.

But I came to my senses and pulled out of the deal.

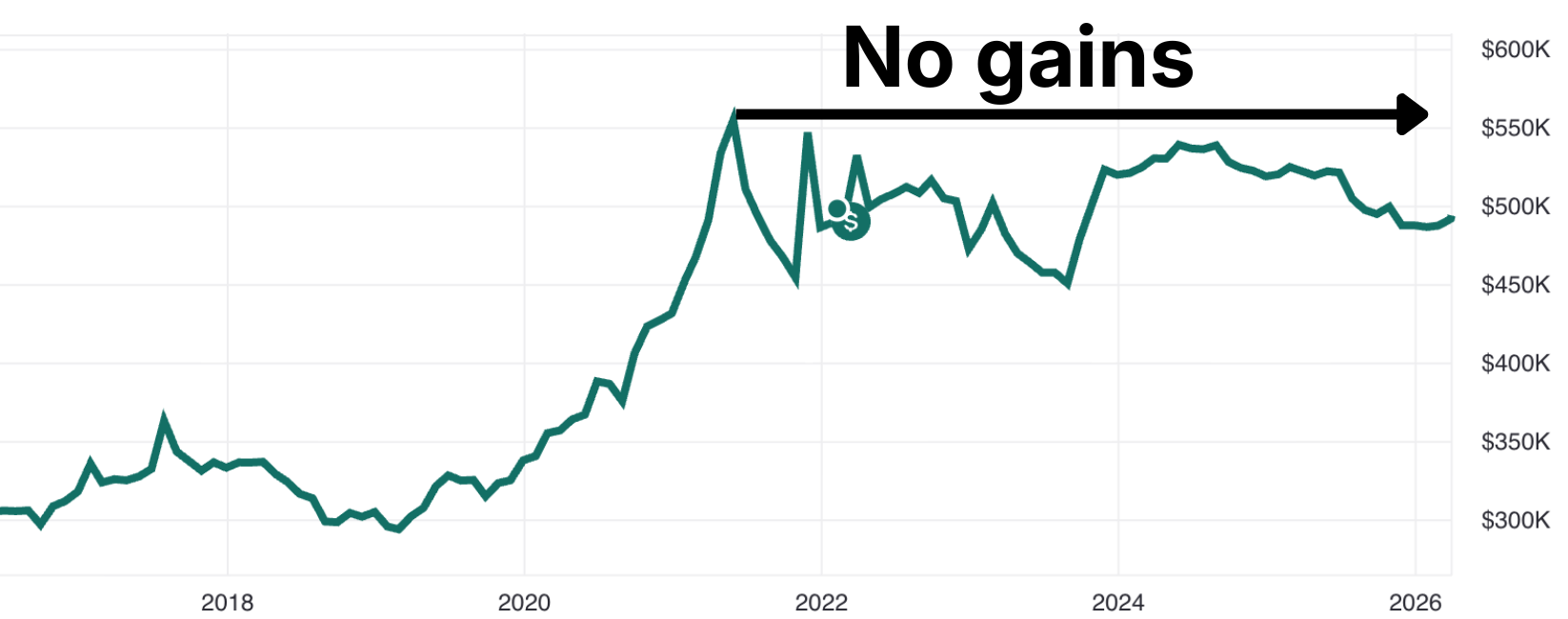

A few weeks ago, I started wondering how that property was doing, so I looked it up. I had offered $510,000 in early 2022. It’s now worth only $493,000 four years later.

Adding up all the costs of negative cash flow, negative appreciation, and comparing the home equity to my stock market investing, that investment property would have lost over -$100k in just 4 years.

Lessons learned

I honestly don’t feel smart for pulling out of that deal. I just feel lucky to have dodged a bullet.

And it was an interesting learning experience about the math and work involved in real estate investing.

My biggest takeaway was just how much time it took. Even tho I didn’t buy the place.

I spent countless hours on market research and financial modeling. Then I spent 15 more hours on the closing process alone. There was driving back and forth to a new city, agent calls, inspection coordination, and loan paperwork.

I spent more time on the closing process than I have managing my entire stock market portfolio over the last 10 years.

Buying my favorite fund takes about a minute. I set up automatic contributions, and the money invests itself. No tax bookkeeping, no tenants, no cleaning schedules, no 2 AM texts about a broken water heater.

It wasn’t just the work that turned me off. I was interested in and willing to do it.

But I was not willing to work more to lose $100,000.

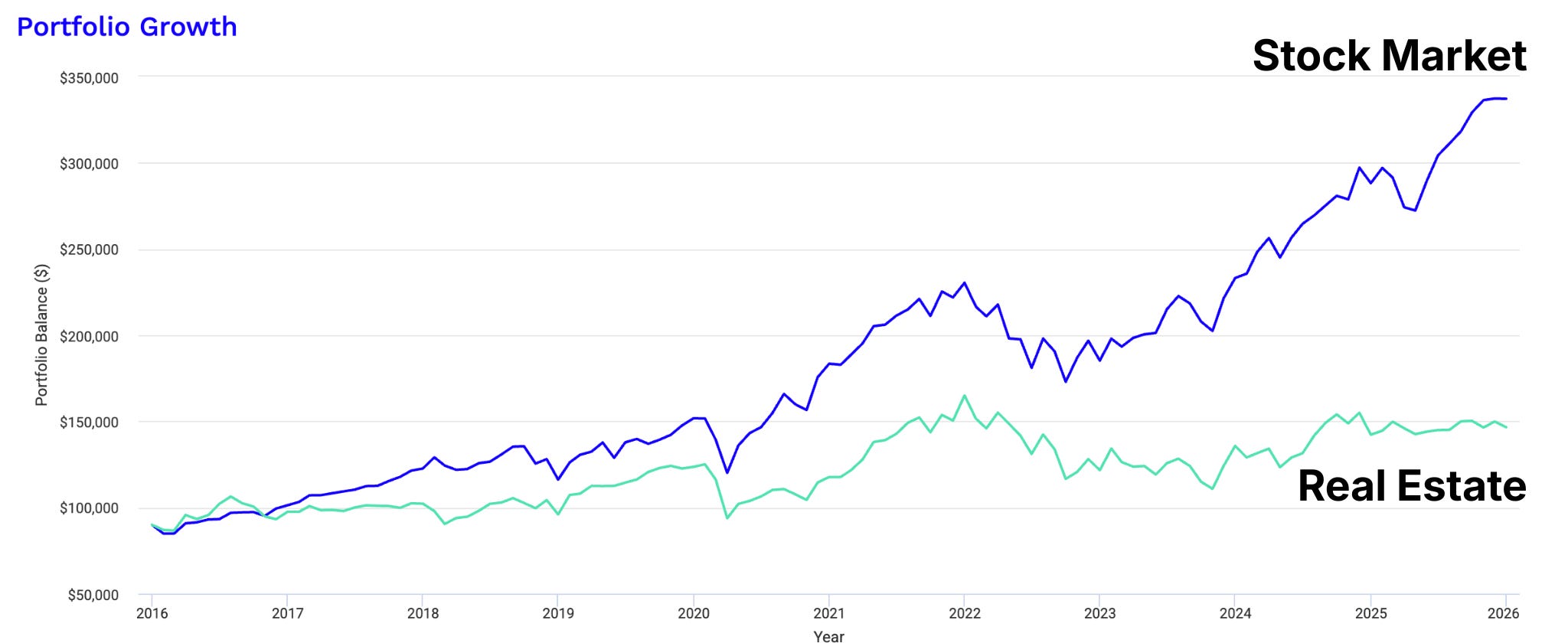

Real estate has not been a good investment over the last 10 years

My property is just one case study. So let’s zoom out and look at the market.

Even the professional, passive version of real estate investing (REITs) underperformed the stock market.

From 2016 through the end of 2025, U.S. stocks returned about +270%, and Real Estate returned about +63%.

I was going to have to spend $90,000 up front to get my property running. That would grow to $337,000 in the stock market after 10 years.

That’s enough to buy a few Porsches. Or take 2 years off for a career break to travel the world.

“But what about leverage and tax benefits?”

I know what you’re thinking. James, you’re forgetting the mortgage leverage. You’re forgetting depreciation. You’re forgetting the 1031 exchange.

I haven’t forgotten any of it. I love nerding out on tax strategies. I modeled the leveraged IRR, cash-on-cash return, and cap rate. I include mortgage interest deductions, depreciation schedules, and equity. Even with every advantage modeled in, the property still underperformed.

I spent hours on it. Financial modeling became a side hustle in itself. Then add to that the job of managing a property and tenants, and it was going to be a lot of work. (My friend who runs Airbnbs assures me that it gets easier once you set up systems, but that’s work too!)

Meanwhile, my VTI fund sat there making more money with zero effort.

Why do we fall for it? When effort ≠ reward.

Investing is the only arena I know of where working harder makes you less money.

Somehow, our brains are wired not to accept this truth.

It goes against everything we’ve been taught. More effort should equal more reward. You get promoted because you outworked people. You earn more because you developed valuable skills. Effort usually always pays off.

So when someone tells you that the best investment strategy is to take 1 minute to buy a fund and never think about it again, it doesn’t feel like enough. It feels like you’re leaving some opportunity on the table because you aren’t working for it.

Combine the ‘effort = reward’ fallacy with the American obsession with land and a heavy dose of real estate FOMO, and you have a perfect recipe for a financial disaster.

However, we need to draw a clear line here. There is a massive difference between a spreadsheet error and an intentional spending choice.

Second homes are fine!

We need to stop conflating investment properties with second homes.

A second home is like buying a sports car. You’re not doing it to make money. You’re doing it for the experience.

Second homes are great. You can expand your life into two locations that bring you joy. It’s hard to imagine a better way to spend your wealth. You can be bi-continental, live by the ocean and the mountains, or balance city life with country relaxation. Go for it!

You don’t need to try to rationalize it because you think it’s a good investment. If you’re buying a life upgrade, that’s great. If you’re trying to build wealth, there are better ways.

Skip the real estate investing.

You simply do not need to own an investment property to build wealth.

If you’re maxing out your tax-advantaged accounts, investing in low-cost index funds, and managing your tax strategy well, you are already doing the highest-return work available to you. My 10 Steps to Life Changing Wealth has the full framework.

Adding a rental property on top of that adds complexity, time, and risk to what has recently been a lower-return investment.

If you still want to buy one after reading this, I respect that. Just run the numbers comprehensively first. Include cleaning, vacancy, property management, maintenance reserves, insurance, property taxes, and your actual time at whatever your hourly rate would be. If it still pencils out after all of that and you want a side-hustle, go for it.

Otherwise, send that cash to an index fund and get back to having fun.

PS. Curious what your down payment would be worth in the market? This link downloads my Excel calculator for that.