If I Started Investing In 2026, This Is What I Would Do (Guide)

Skip the stock-picking stress and learn the exact 5 steps I would take to go from zero to a fully automated, tax-advantaged investment portfolio.

Going from $0 to your first $1,000 invested is often harder than going from $10,000 to $100,000. Not because the steps are difficult, but because there is a big psychological barrier to cross when you first put your money at risk.

It’s easy to wonder:

What should I do first?

How do I make sure I don’t miss something?

How do I know if I am choosing the right investments?

Is now even a good time to invest in the market?

In this article, I boil down the answers to these questions and more. I walk through exactly what I would do if I were starting from scratch today, using what I’ve learned from two decades of investing and financial planning for global organizations.

Let’s get started.

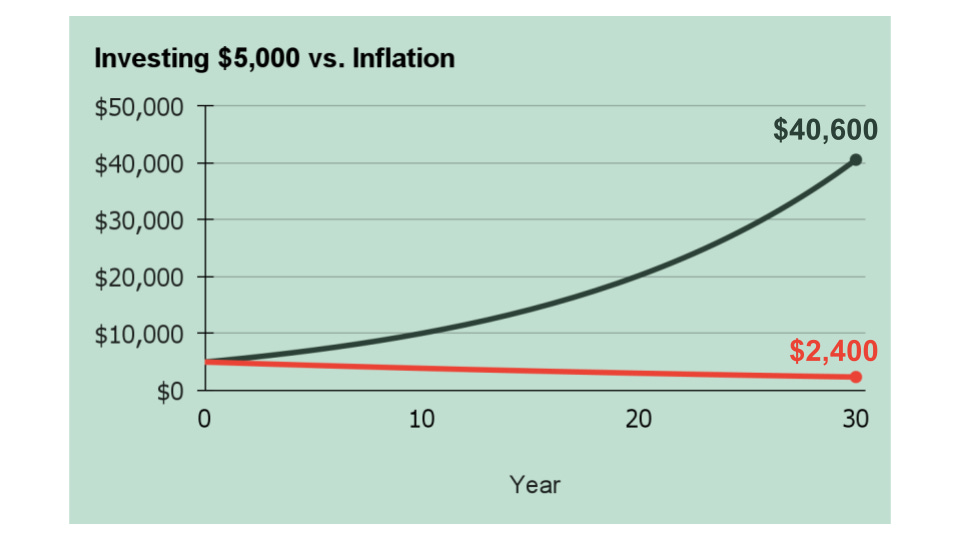

Starting early matters more than almost anything else. It gives you time to build skill, confidence, and momentum as an investor. More importantly, it gives your money time to compound.

Because when money sits uninvested, it’s getting eaten by inflation. For example, $5,000 invested for 30 years at a 7% return could grow to about $40,600. But uninvested, an inflation rate of 2.5% would reduce the value to $2,400.

Step 1: Check That You Are Ready To Invest.

Before I invest seriously, I would make sure I am not passing up free money, carrying expensive debt, or one small emergency away from selling investments. Taking care of those first would make me wealthier in the long run, so I would not skip them.

Capture your employer match first, always.

I’d grab my employer’s 401(k) matching contributions before anything else. That’s free money and an immediate 50% to 100% return.

Pay off high-interest debt next.

I’d eliminate any debt above 7% interest, like credit cards, payday loans, and personal loans. Paying off a 20% APR credit card is a guaranteed 20% return. That’s much higher than average stock market returns.

Have a small emergency fund.

This may be a controversial opinion, but I would not wait to have the often-recommended 6+ months of expenses in a savings account before starting to invest. That would just delay investing too long. Instead, I would start investing as soon as I had enough cash available to cover day-to-day surprises (e.g., a car repair) so that I don’t put myself in a pinch.

Step 2: Pick One Of The Major Brokerages

Now I’m ready to invest. I would first choose one of the major brokerages for my investing: Fidelity, Schwab, or Vanguard. I would not overthink this because they are all excellent. They’re low-cost, well-run, and have been around long enough that I would not worry about using any of them.

I already have accounts at all three, but do over 75% of my investing through Vanguard. If I were starting over, I might choose Fidelity because the interface is a little easier than Vanguard, and more of their funds have no minimums. But I’m splitting hairs. I love them both.

Step 3: Open The Right Account

If you want to build true wealth, understand how to save on taxes. And tax-advantaged accounts are your first line of defense.

A tax-advantaged account lowers taxes either when money goes in or when it comes out. The main types are IRAs, 401(k)s, and HSAs, and they usually come in two versions:

Roth: You pay taxes now and withdraw tax-free in retirement

Traditional: You get a tax break now and pay taxes when you withdraw later

As a general rule, invest first in tax-advantaged accounts. After maxing out those, move on to taxable accounts.

I would start by opening a Roth IRA account. In a Roth IRA, contributions are made with after-tax dollars, growth is tax-free, and qualified withdrawals in retirement are tax-free. It’s one of the best long-term advantages available to investors.

However, high-earners can’t contribute directly to a Roth IRA. If you make more than $153,000 for single tax filers or $242,000 for joint tax filers in 2026, you have to go through the backdoor Roth IRA process. It’s a few extra steps, but it’s worth it. I’ve written a full guide to that here. The process is to contribute to a Traditional IRA and then convert those dollars to a Roth IRA.

The account type determines how you are taxed, but not what you own. That choice comes next.

Step 4: Buy One Low-Cost Fund

Many people get stuck on choosing from thousands of potential investment options and then figure out how to combine them into the perfect portfolio.

If you enjoy that kind of thing, go for it. But it’s entirely unnecessary. It will just suck up your time without increasing your expected returns.

Instead, I would simply buy a single low-cost stock market index fund. These funds hold thousands of companies across every sector and size. You get to own the entire market instead of betting on individual pieces of it. It’s simpler and gives you a better chance of matching market returns at a very low cost. See my favorite fund here.

A few things worth knowing:

Low-cost: Expense ratios matter over long time horizons. A fund charging 0.03% is dramatically cheaper than one charging 0.5%. That difference can easily cost you tens of thousands of dollars over 30 years.

Stock-picking is nearly impossible to win. More than 75% of professional fund managers fail to beat simple index funds over 15 years. For a non-professional, it’s even harder.

Bonds are optional to start. You don’t need bond exposure on day one if you are still many years from retirement. But if you want it, allocate a portion of your investing to a low-cost fund like Vanguard’s BND or Fidelity’s FXNAX.

I’d pick a low-cost diversified index fund like VT or VTI and invest the first dollar.

Step 5: Automate It And Stop Thinking About It

This is one of the simplest ways to “pay yourself first”.

Set up a recurring contribution to run automatically. It could be weekly, biweekly, or monthly: whatever matches your paycheck schedule is usually easiest.

For example, someone paid semi-monthly could time their automatic investing to match one paycheck each month and their mortgage to the other, since those are usually the biggest cash needs.

Why set this up? Automating does three powerful things.

It removes the decision entirely. You don’t have to remember to do it, and you can’t talk yourself out of it when the market dips.

It smooths out your entry points over time, so you’re buying at a range of prices rather than all at once. This is called “dollar cost averaging”.

It takes money out of your checking account quickly, helping prevent impulse purchases and lifestyle inflation.

Start with whatever amount you can. Even $100 a month is enough to build the habit. Increase the amount when you get a raise. The system grows with you.

The goal would be to make investing automatic, not something that depends on willpower each month.

The Final Hurdle: Don’t Wait For The Dip.

As I write this, market valuations are still fairly high despite recent volatility. The mood is a mix of optimism and pessimism. On the positive side, the tech giants are still making big investments in AI, funded by strong profits. On the negative side, geopolitical uncertainty, rising prices, and fears of a bubble are worrying many investors.

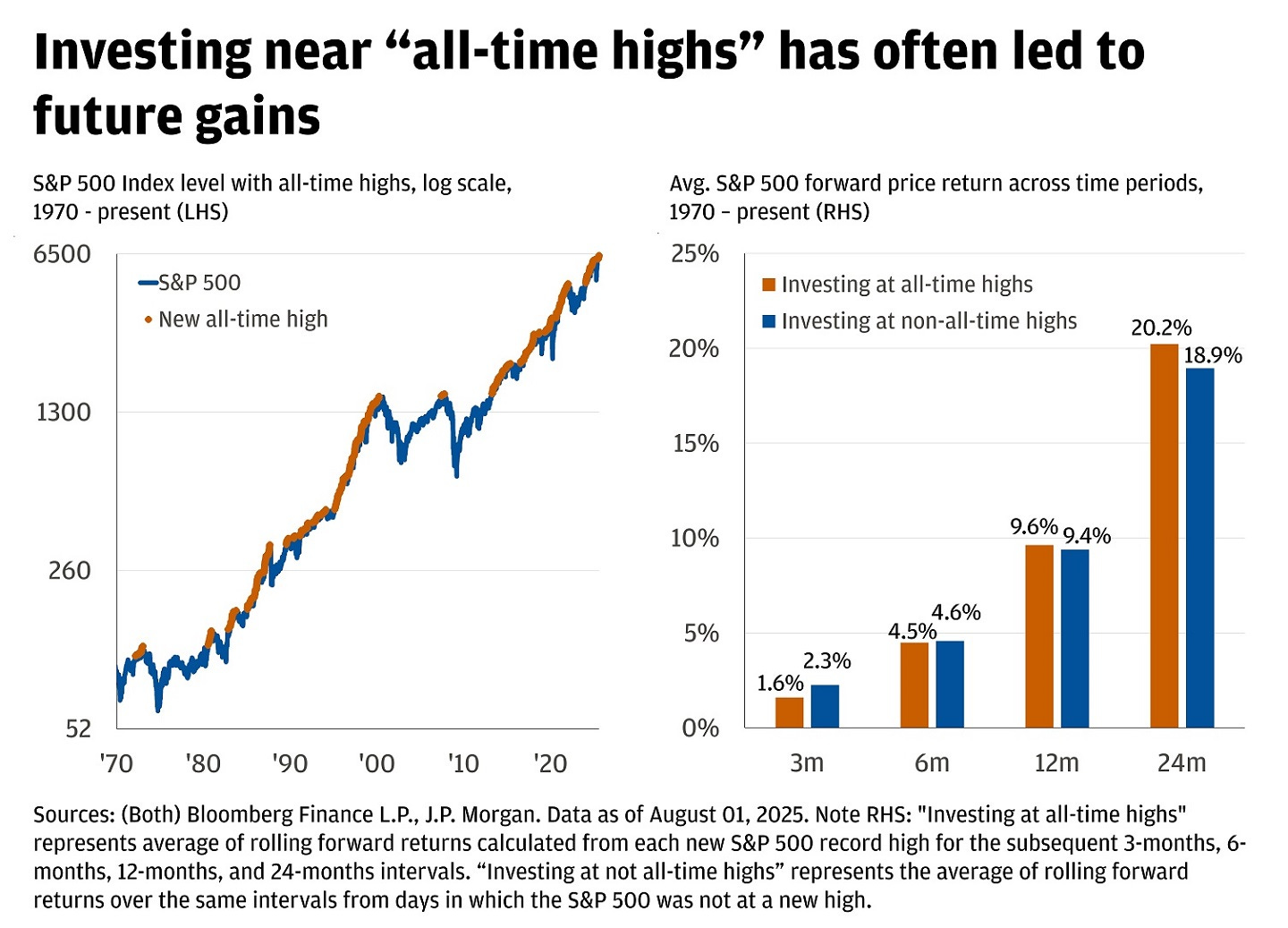

Let’s start with looking at the fears of a bubble or that the market’s all-time highs mean we are ‘due’ for a correction. The high valuations may seem scary, but they are very common. Consider this analysis by JP Morgan1. Even when people invest at all-time highs, they tend to perform better over the next few years.

Maybe stocks are on the decline as you read this, and you think: Should I wait for the dip to go lower? It may sound reasonable. But in practice, it usually means sitting out while other people make money.

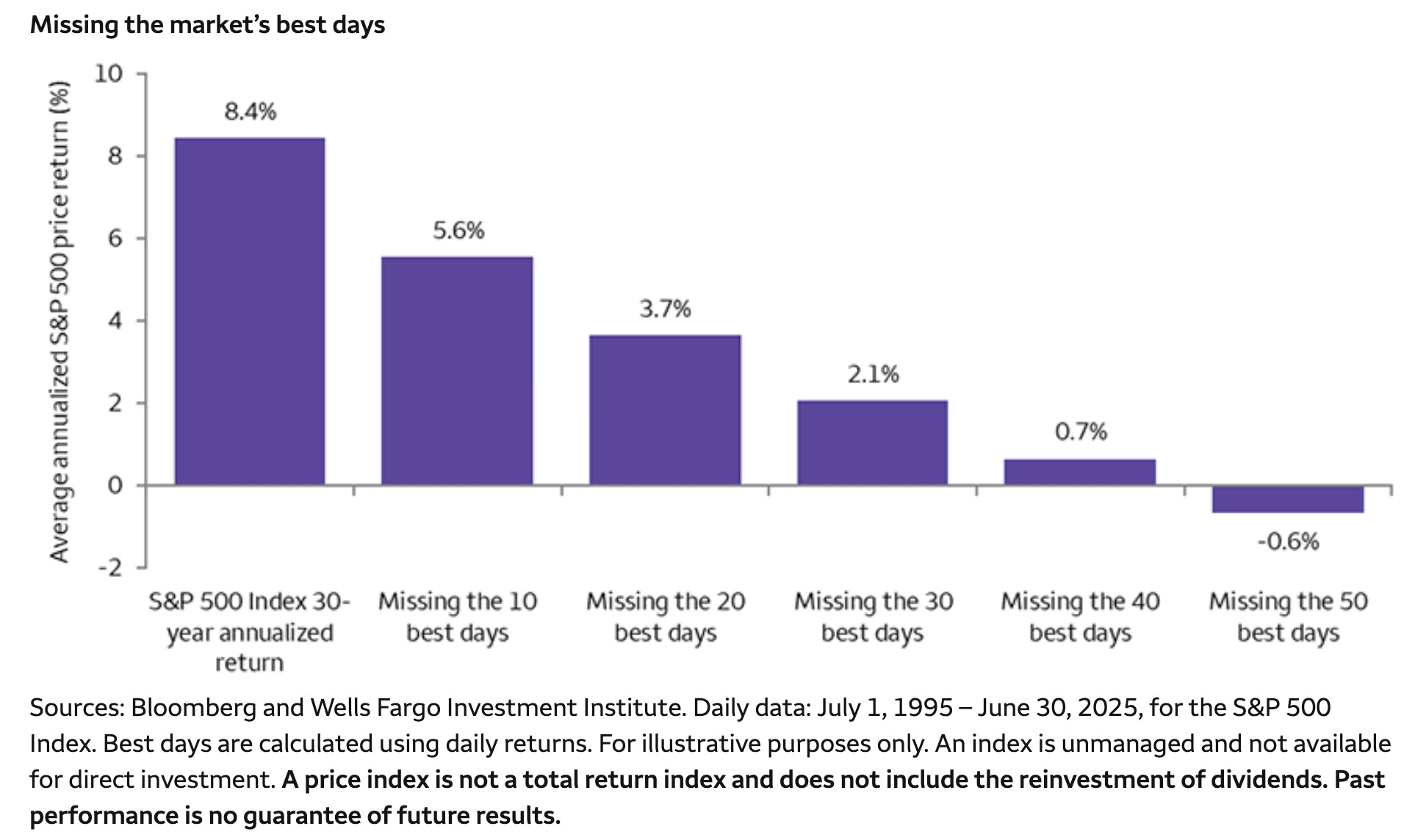

When you are sitting on the sidelines, you could be missing some of the market’s best days, and that matters a lot. The research below from Wells Fargo shows that missing just the best 10 days in a 30-year period would cut your return by a third, from 8.4% to 5.6%, and it gets worse from there2.

Even investors who bought right before major crashes like 2000, 2008, and 2020 recovered and then some, as long as they stayed in. The holding period is what matters. Over any 20-year window in modern market history, a diversified index investor has come out ahead (yes, even during the great depression3).

Investing success comes from investing early and staying invested, not from trying to perfect time entry points.

If you’re still uncomfortable putting money in right now, make the amount smaller and invest once a week to get into the market slowly over time.

Get started today.

You do not need the perfect plan. You need a simple system. The goal is to get invested and stay invested.

Get the basics in place

Open an account at a brokerage

Buy a low-cost diversified fund

Automate the habit

Don’t wait for the perfect moment to start

That’s it! Everything else can come later, while the system is already running.

A straightforward investing system started today can easily change the rest of your life.

Keep going: Ready for the full playbook? Here are my 10 Steps to Life Changing Wealth, covering everything from your 401(k) to tax-loss harvesting. Earning above $150K? You need to know how to do a Backdoor Roth IRA the right way before you invest in a regular IRA.

Disclaimer: This article is for general education only. It isn’t personal financial advice. I don’t know your full situation, goals, or risk tolerance, and nothing here should guide your decisions on its own. Do your own research or speak with a professional before acting on any investment ideas.

https://www.jpmorgan.com/insights/markets-and-economy/top-market-takeaways/tmt-slower-growth-higher-inflation-and-s-and-p-five-hundred-all-time-highs?utm_source=chatgpt.com

https://www.wellsfargoadvisors.com/research-analysis/reports/policy/volatile-markets.htm

https://fourpillarfreedom.com/heres-how-the-sp-500-has-performed-since-1928/