How much you need to retire. Finally a simple answer.

Figure out the one number you need to be financially independent. It takes less than 1 minute.

When people come to me for financial consulting, I’ll eventually ask them how much they think they’ll need to retire.

“Well, I never really thought about it. Maybe a couple million? Is that enough? Do you think I need more?”

In seconds, doing 5th-grade math, we figure out their number. In another 5 minutes, we can usually tell if they’re on track to hit that.

At that point, they’ll usually say something like: “Wow, that feels really good to know I’m on track. I had no idea.”

It’s one of my favorite things to see the happiness and relief they get from now understanding where they are in their financial journey.

After today, you’ll be able to do the same.

The magic number is 25x.

It’s 25x your annual spending.

The math is surprisingly simple.

Take what you spend in a year. Multiply by 25.

That’s it. That’s the size of the portfolio you need to retire.

Annual spending x 25 = Retirement number.

Your annual spending is what you expect to need in retirement. And if you are not sure what you expect to spend in retirement? Just use your current spending!

Your current spending is generally a very good approximation. You will have some spending go up in retirement (e.g., healthcare), and some go down (e.g., commuting). We know from research that most people’s spending declines in retirement, even after accounting for health care and other new costs. So your current spending is conservative.

Spend $120k a year? You need $3 million.

Spend $100k? You need $2.5M.

Spend $80k? You need $2M.

You can see why $1M ain’t what it used to be.

The 25x number works very well for planning when you are still many years from retirement.

Note - if you are very close to retirement, you will want to build a more complete financial plan, factoring in your specific situation, including Social Security, medical costs, etc., and that gets much more complicated. As in - custom tools with break-even analyses, tax-rate smoothing, and Monte Carlo scenario modeling. I love that stuff, but I don’t recommend it for people who aren’t overanalyzers like me.

The 25x number is tried-and-true. It’s straightforward, yet still effective because it’s based on a mountain of financial research and data analysis.

Why the 25x works. Aka the 4% rule.

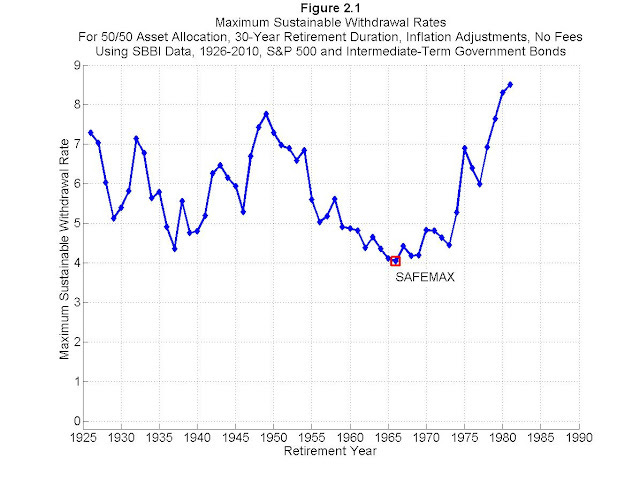

In 1994, a financial planner named William Bengen ran the numbers on every 30-year retirement window in U.S. history going back to 1926. He wanted to know: what’s the highest withdrawal rate that would have survived any retirement date, including the Great Depression, the stagflation of the 1970s, and every bad event in between?

The answer was 4%. A retiree who started by withdrawing 4% of their portfolio in year one, then adjusted that amount for inflation each year after, would have made it through every good and bad 30-year retirement period.

A few years later, three professors at Trinity University ran a similar study with broader data and confirmed it. The 4% rule has been tested, retested, and stress-tested for thirty years. It is one of the most thoroughly examined ideas in personal finance1.

Using the 4% safe withdrawal rate from their research, we can again use simple math to figure out how much we need to save.

4% is just the inverse of 25. 1 divided by 4% = 25. Which means,

If you can safely pull 4% a year to cover your annual spending, then you need 25 times your spending in your portfolio.

It has a few minor caveats. The most important thing is for people who are retiring early. If your money needs to last 50+ years instead of 30, some people choose to be more conservative and choose a withdrawal rate of 3.5%, which is equivalent to 28x. My Google Sheet calculator can adjust the withdrawal rates to see the impact of that choice.

For most people planning a normal-length retirement, 25x is the number.

Use it as a tool, not just a target

This concept is powerful because you can now use it as a tool to understand and make spending decisions, knowing how they affect your entire life plan.

This is a big level-up in your financial thinking. Most people are thinking in terms of what they can afford from their current paycheck or, at best, their annual salary.

You can now see how increases or decreases in spending and saving affect your entire life.

When we look at 25x as a tool, we can see that it’s a lever you can pull from both ends.

Most financial advice focuses on saving. Save more, invest more, contribute more. That’s important, but it’s only half the equation.

The other half is the spending side.

Watch what happens when you change your spending:

Spend $120k → need $3M

Spend $100k → need $2.5M

Cutting $20k of annual spending didn’t just save you $20k. It cuts $500k off your retirement target.

Every dollar you cut from your annual spending reduces the portfolio you need to build by $25. That’s a big lever!

It helps us understand another powerful concept: savings rate. The savings rate is the percentage of your income you save.

Changing your savings rate moves both sides of the 25x number simultaneously.

When you save a higher % of your income, you’re spending less, which lowers the amount you need and contributes more. You can retire faster.

The early retirement/FIRE movement built its whole strategy on this insight: a person saving 50% of their income can retire in roughly 17 years, regardless of whether they earn $80k or $300k. It’s the % of savings rate that matters most.

Use this easy calculator in Google Sheets to see if you are on track. It takes 2 minutes. Then see what happens when you adjust how much you spend and save.

Designing the life you want

Once you understand 25x as a tool, you can ask much more interesting questions like “what kind of life do I actually want now and later?”

If you use the calculator and find you are already on track to retire, you have options most people never realize they have.

You could keep saving and retire earlier. That’s the obvious one.

Or you could spend more now! If you’re going to overshoot your number anyway, what’s the point of overshooting it by a lot? Spend the extra money on things that actually matter to you while you are active enough to enjoy it.

Dream vacations. A kitchen renovation. Whatever you’ve been deferring.

You could take a career break or sabbatical. If your portfolio is large enough that it’ll grow to your 25x number on its own without further contributions, you can stop saving for a year or two without derailing your retirement.

Round-the-world trips, time at home with kids, a stretch to write the book or start the business. These become real options.

You could switch to consulting, launch a business, or go part-time in the future.

The math doesn’t care whether you make $500k a year or $100k. It cares whether you are on track to hit your number.

The point of financial mastery isn’t to hit some number in a spreadsheet. It’s to design your life, both now and later.

The lesson for mastering your finances

You can master your finances by understanding just a few core concepts and using tools to put them into practice.

This is one of those core concepts. So take two minutes with this calculator.

You’ll land in one of three places. You’re behind, you’re roughly on track, or you’re ahead. Each one tells you something useful and gives you choices.

Most people walk around with a vague, low-grade anxiety about their finances.

They never quite know if they’re doing enough.

They earn well, save reasonably, and still feel uncertain. That feeling doesn’t come from their actual situation. It comes from not understanding their own specific number.

Once you have your number, you know where you are. You know what your options are. And from there, you can stop optimizing for some abstract future and start designing the life you actually want.

If you want to really fall down the analysis rabbit hole of Safe Withdrawal Rates, see EarlyRetirementNow.com’s 63-part series. He’s run the calculations in nearly every situation imaginable. I love them, but they are not light reading.

A strong piece an a a very useful way to simplify the question. Simplicity matters.

I think the next layer of clarity comes after the 25x number: understanding what part of that future income needs to come from your portfolio at all.

For many people, a pension may already cover part of that number. So the real job is not just finding the number, but identifying the gap and building calmly towards that.

Calculation works both ways. The other way of thinking about it is how much could I spend per year if I retired now? Answer = current savings / 25. The benefit of that frame is seeing how much your financial freedom lifestyle grows as you increase your savings.