Ignore the influencers: index vs. income strategies after tax

A breakdown of dividend and covered call ETFs vs. index funds, compared on after-tax returns.

I love that more people are learning to invest online. They’re trying to educate themselves on how to build wealth and set up their financial future.

A few decades ago, the biggest challenge was getting access to information about investing.

Today, the challenge is too much information.

There has been an explosion of advice and investment options. And half of that advice is coming from an influencer with a yield chart but no mention of what you’ll owe the IRS.

Nowhere more so than in the incredible growth in stock market Exchange Traded Funds (ETFs). There are now over 4300 ETFs in the USA. More than the number of individual stocks they are often buying!

Stock market ETFs are pooled investments that hold a group of individual stocks. They are nearly equivalent to mutual funds with some minor differences, the most important being that you can trade them on the open market.

You can design ETFs to serve just about any market strategy you can think of.

When you buy an ETF, you’re buying the investment strategy of that fund and the taxes, fees, and risks that come with it.

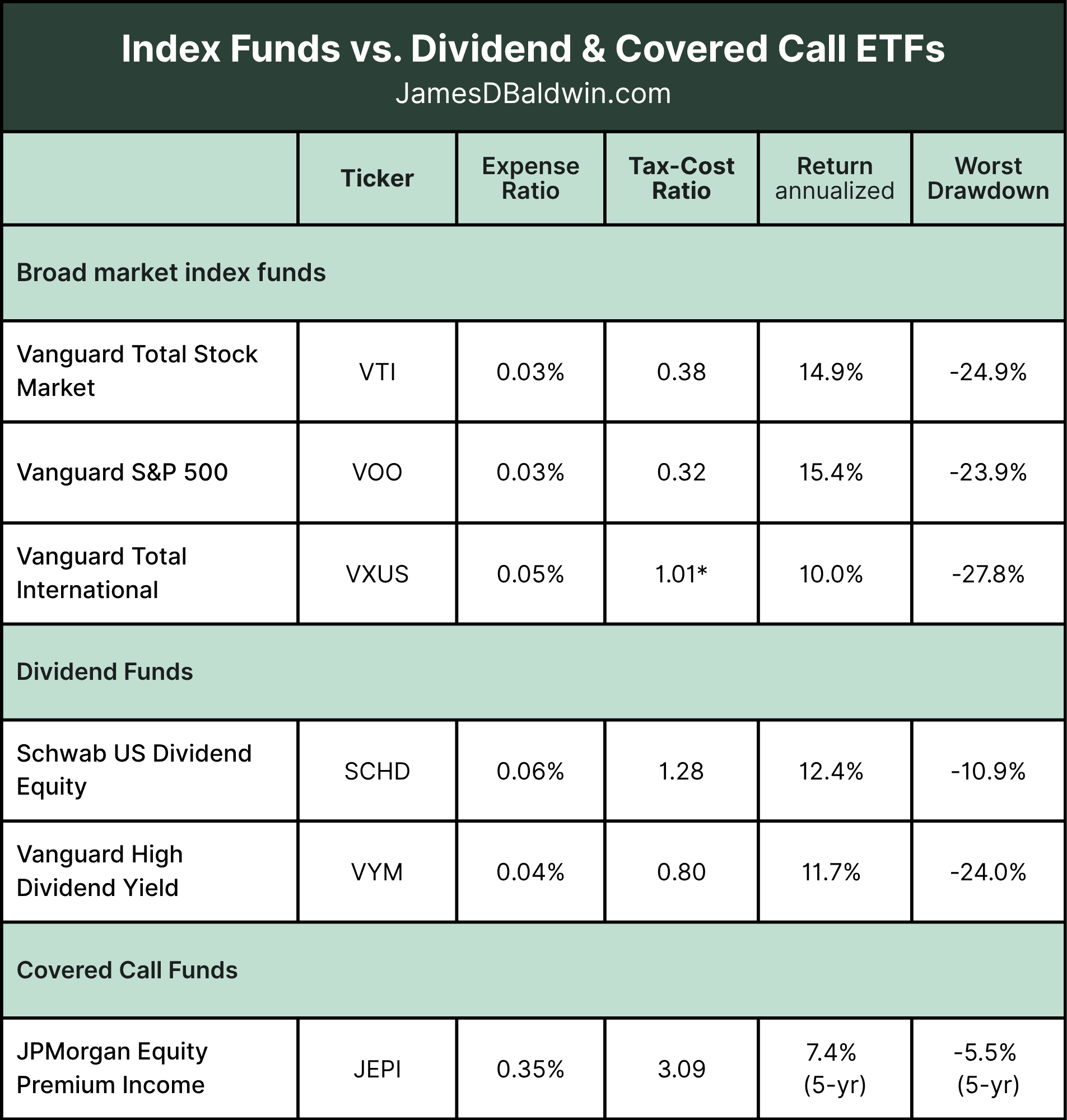

ETFs can vary drastically and the details matter. For example, the ETF JPMorgan Equity Premium Income (JEPI) costs about 8x more in taxes than an broad index ETF.

Today, I am going to look at the most commonly recommended ETFs that promise more income and safety to understand the non-obvious risks, costs and benefits of each. (See the table at the bottom for a full breakdown of each).

I’ll give a breakdown and verdict on each, comparing their last 10 years of performance to the gold standard of investing - broad stock market index funds.

The two primary income strategies are:

Dividend Funds

Covered Call Funds

The Framework: Risk vs. Return after taxes & fees

We’re going to look at these ETF strategies from someone whose goal is portfolio growth so they can build long-term wealth over the next several decades. This is very different than someone who is in or approaching retirement and has different goals and priorities.

What matters is not how much you make, it’s how much you keep. Every dollar you keep by avoiding taxes and fees is a dollar that keeps compounding.

Similarly, you need to protect yourself from the big risks that will take you out of the game completely.

These funds are still fundamentally vehicles for multiplying your money. You’re buying them to grow your wealth. But once you’re choosing between funds with similar growth goals, the difference in what you keep is what separates them.

This is particularly important for people in high tax brackets where avoiding taxes matters more.

Broad index funds: the gold standard

Before we get into the two funds, let’s take a moment to understand why these are our benchmark and the gold standard of equity investing.

Broad Market Index Funds simply buy up all of the stocks in the market, or a significant part of it.

They are ultra-low cost, often <0.1% because they don’t require a lot of staffing and management overhead to run the fund or analyze their strategy. The strategy is dead simple. In the case of Vanguard Total Stock Market (VTI), the strategy is to buy every major stock in America and hold it.

They are also inherently tax efficient because they’re not constantly buying and selling stocks. Other ETF strategies have more frequent sales, each of which can create capital gains taxes.

The three benchmark funds all generated healthy double-digit returns with their worst drawdown in the last 10 years comparatively smaller than other stock funds.

Vanguard Total Stock Market (VTI) is the most diversified of the group, so if you’re looking to invest across the entire U.S. market, that’s the option to go with. It’s also my favorite fund.

Vanguard S&P 500 (VOO) buys just the largest 500 or so U.S. companies, but functionality is nearly identical to VTI since the largest companies in the US dominate both funds.

Vanguard Total International (VXUS) buys the most important companies outside of the U.S. It’s a natural complement to the other two funds if you’re looking to add some international stocks.

VERDICT: These VTI, VOO, VXUS are funds we are happy to buy and own them anywhere. Low fees, low tax drag, standard volatility while you get the expected return of the whole market. Hold these in any account you have - either a taxable brokerage or a tax-advantaged account like a 401(k).

Dividend funds: if it sounds too good to be true…

At first glance, Dividend Funds sound appealing. They filter for stocks that pay comparatively higher dividends. The idea is that you get the growth potential of stocks, with reliable income from dividend as well.

Dividend funds essentially look for all the companies that prioritize returning profits to investors as dividends now, rather than using the profits to reinvest in the company with the intention of growing the company profits and stock price in the future (Growth Funds do the latter.)

If you are a long-term investor, should you prefer dividends over stock price growth?

If we’re investing for the long term, we don’t care if we get the profit now or later. We simply want to maximize wealth growth.

You have to pay a slightly higher price - in the form of higher taxes - to get dividend income. Some dividends are qualified, meaning they’re taxed like capital gains the same as any stock growth, but some are not.

That makes taxes on these funds two to four times higher than the index funds.

The other major downside is that these funds don’t buy all of the market. They exclude industries and companies that don’t pay much in dividends, like tech, for example. Tech businesses’ massive growth has driven huge stock market gains in recent years. For that reason, dividend funds have underperformed the market 3-4%.

On the upside, there is some truth to these stocks performing slightly better in down markets. But when the market’s down, their prices are down too. Their promise of more safety only is true during smaller declines when the market rebounds quickly, not in the big stock market crashes that are the real risks.

Let’s look at the two frequently recommended funds

Vanguard High Dividend Yield (VYM) had a very similar drawdown to the overall market drawdown while underperforming the market and paying higher taxes.

Schwab US Dividend Equity (SCHD) also underperformed the market and paid higher taxes, but had much less volatility and a smaller drawdown. However, this is due to SCHD having stricter criteria for which companies it buys. It’s not the dividend itself that makes the fund less volatile.

VERDICT: skip VYM, SCHD, and dividend funds. You already own these companies inside a broad index fund like VTI. You’re not gaining diversification, you’re paying slightly more in taxes for less growth, and a little less volatility. Even in a tax-advantaged account, you’re still holding a fund that’s underperformed the index by 3-4% a year.

Covered call funds: less upside + more taxes

The goal of the covered call strategy is to use stock market exposure with some complicated financial engineering to generate a steady income with less volatility.

Covered call funds own stocks, and then also sell call options against them. They are selling away the rights to some of their potential future gains if those stocks rise above a set price. The fund collects the cash from selling that option and pays it to you as monthly income.

On the upside, these funds pay more regular income than dividend funds, and the premiums cushion the fall when markets drop which leads to smaller drawdowns while you receive some steady income.

However, these funds generate up to 10x the taxes of an index fund. Covered call payouts mostly don’t qualify for the lower dividend rates. They’re ordinary income at your full marginal rate. Someone in a high tax bracket might only keep 60% of the income from this fund each year. Compare that to an index fund that lets gains compound nearly untaxed until you choose to sell. These funds hand you a tax bill every month whether you need the income or not.

The other big problem is that you miss out on big gains in the market because the funds are selling those away for income. You keep most of the losses and sell off the big gains. Markets rise most years, so you’re trading decades of compounding for income today.

JPMorgan Equity Premium Income (JEPI) is often recommended in the category. It returned 7.4% a year over the last five years, lower than the overall market. Its tax cost ratio of 3.09 is about eight times VTI’s, and its worst drawdown was just 5.5%.

VERDICT: Skip JEPI and covered call ETFs. Index funds are a better option for the growth part of your portfolio. If you do buy these, put them in an IRA to avoid heavy taxes.

Neither income strategy beats the index in terms of expected return, and both cost you more in taxes to get there. If your money’s goal is growth, not monthly cash flow, VTI does the job better than either one.

If you own a dividend or covered call fund right now, pull up its tax cost ratio and see what it’s actually running you.

The Single Best Investment for Long-Term Wealth.

Have money to invest that’s been sitting on the sidelines for a while? Not sure where to put it?