Most Investors Made Money in 2025. Did You?

The quilt chart shows why chasing last year’s winner is one of the most expensive mistakes investors make.

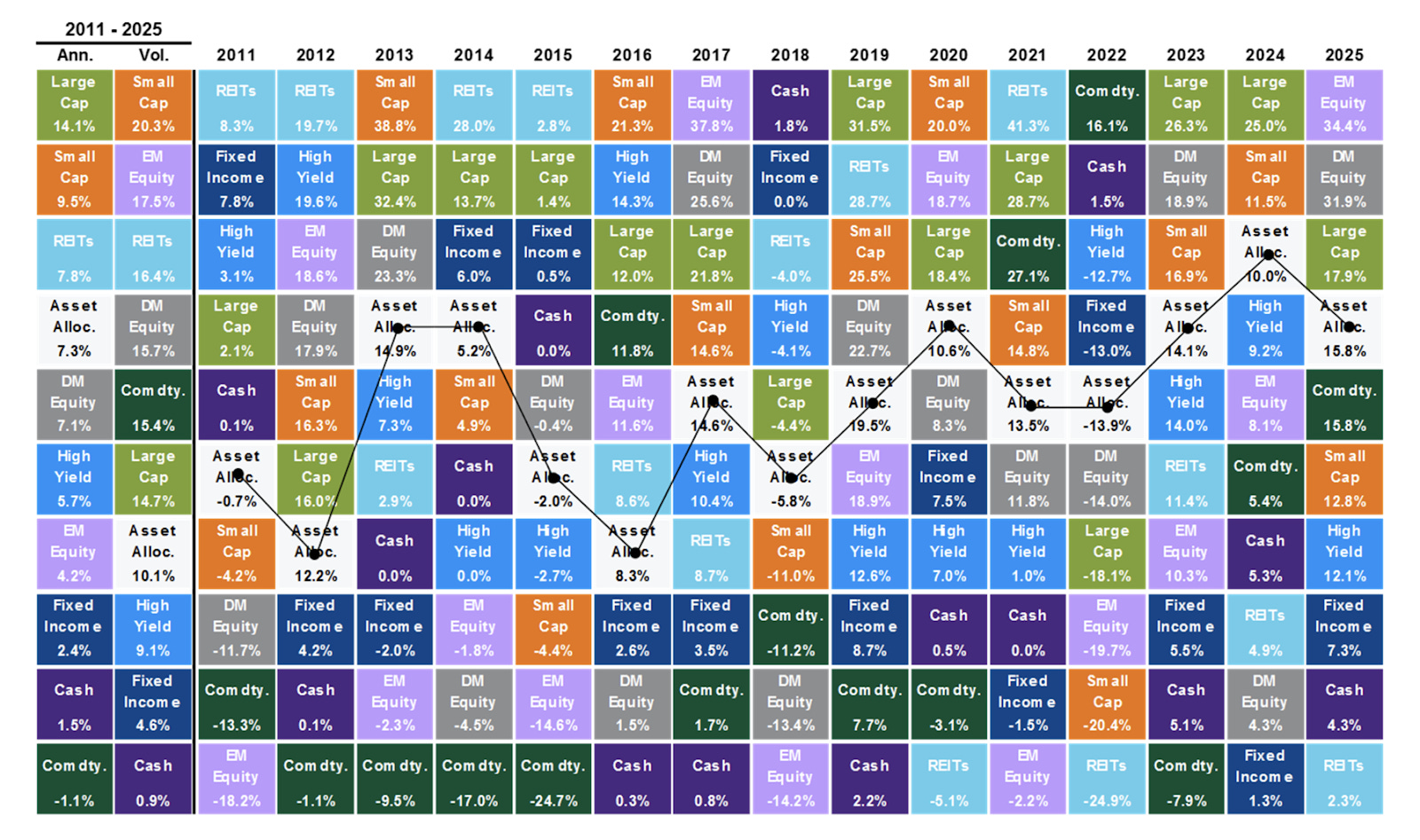

This is one of my favorite charts. It’s my annual reminder to stay diversified.

Each year, JP Morgan publishes this “quilt” in their Guide to the Markets1. It ranks major asset classes2 from best to worst based on annual returns, going back 15 years.

2025 was a strong year across most asset classes.

International equities (stocks) did very well. Money rotated out of the US into other markets, and the US dollar weakened significantly. Large cap US equities also stayed on a hot streak.

If you were broadly invested, you likely did fairly well in 2025.

What Does This Tell Us About The Market?

Zooming out and looking at the full chart, it’s hard to discern any reliable patterns.

The top performer one year was sometimes near the bottom the next. The worst performer could become the best when market cycles changed.

Take emerging market equities. They led all asset classes in 2017 at 37.8%. In 2018, they were dead last at -14.2%. Then they had several mediocre years. In 2025, they led the pack again.

Large cap equities have been the most reliable asset class over the last 15 years. They ranked in the top third of returns in 11 of those years. Even so, they still had a poor year during the 2022 bear market.

Once again, we see that the market is unpredictable from year to year.

Despite that, we consistently see positive results when we look at the 15-year returns in the far left column of the chart. There has never been a 15-year period in which the S&P 500 has had negative total return.3

Consistently investing pays off without requiring the best performance in any given year.

Reality Doesn’t Match What You Read

The short-term unpredictability generally doesn’t show up in what you read online.

News coverage focuses on extremes. Influencers are rewarded for promoting something different. Usually, it’s a “secret” investment they claim to have figured out first. Things like crypto, micro-caps, gold, and silver.

The assets that dominate online are rarely the ones that are actually building the most wealth for investors.

Be cautious of focusing on recent performance or narrow investment advice. That’s how people end up chasing returns.

Refer to the chart above. Yesterday’s winner often becomes tomorrow’s loser. The result is poor returns, higher taxes, and an emotional roller coaster.

Play A Different Game. Always Win In The Long-Term.

You can sidestep the game of return-chasing entirely by building a diversified portfolio of stocks and bonds.

You won’t ever have that year’s best returns. But you’ll consistently be in the top half.

That’s like getting a bronze medal at the Olympics. If you get on the podium every year, you’re still doing better than the vast majority of people.

Thankfully, that’s all you need to do to build real wealth.

Here’s how:

Buy low-cost broadly diversified index funds.

Buy a stock fund. Great options include: VTI for US stocks (my favorite fund), VT for total world stocks, and/or VOO for the S&P 500.

Plus buy a bond fund. I use BND.

Base your bond allocation on your time horizon.

Then set a calendar reminder to rebalance your portfolio once a year.

That’s it. You’re done. Go back to living life and going on adventures.

Benefits of a diversified strategy:

It’s much simpler. It requires fewer decisions and less effort. You set an allocation and stick to it. No debating the exact right time to buy or sell.

Lower stress through lower risk and volatility. Investments always have ups and downs, but diversified portfolios mute the wildest swings.

You save on taxes from trades. Holding index funds minimizes capital gains taxes and lets more of your return compound.

Diversification works because it removes the need to be right about what comes next.

You automatically own the winners when they emerge, without trying to predict them ahead of time. You also own the laggards, but that’s the trade-off that lets your portfolio grow with a rising market without return-chasing and with less risk.

The goal isn’t to predict the next winner. It’s to avoid being wrong in ways that permanently set you back. If you do that for long enough, the result takes care of itself. You will build life-changing wealth.

PS. If you want to play along, make a prediction in the comments about which asset class on this list will do best in 2026. We can see how we do in a year. Odds are, it will be humbling.

Disclaimer: This article is for general education only. It isn’t personal financial advice. I don’t know your full situation, goals, or risk tolerance, and nothing here should guide your decisions on its own. Do your own research or speak with a licensed professional before acting on any investment ideas.

https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

All data represent total return for the stated period. The “Asset Alloc.” box cutting through is a hypothetical diversified portfolio of 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg U.S. Aggregate, 5% in the Bloomberg 1-3m Treasury, 5% in the Bloomberg Global High Yield Index, 5% in the Bloomberg Commodity Index and 5% in the NAREIT Equity REIT Index.

Crypto isn’t included in this quilt. BTC was down -6.3% in 2025.

https://petersonwealth.com/webinars_category/investing/ Note that this is true in nominal terms. I couldn’t find a source that verified it in real terms. I suspect there have been some periods around the 70s and potentially 2000s where it may have been flat or negative in real terms. I haven’t had time to run the numbers. If anyone has a source for this, please share!