Most high earners park cash in the wrong place.

The highest-yield account is rarely the most after-tax yield. Here's the real rankings, by bracket.

This is a follow-up to “Most People Park Cash in the Wrong Place,” which was aimed at all savers. This follow up is for high earners or people who live in a high-tax state.

I get this question frequently:

“Where should I put a big chunk of cash to get the highest safe return?”

If we are high earning or live in a high-tax state, it’s not as simple as choosing the account with the highest interest rate.

As the saying goes, it doesn’t matter what we make, it’s what we keep.

To know how much we keep, we have to consider my favorite frenemy: taxes.

It is our after-tax return on our savings that matters. And the more you make, the more it matters.

Understanding our options

We’re looking at a use case where we want to keep our cash safe. This could often be for a down payment or some big expense you’re expecting soon. This isn’t money we want to invest for the long term.

We have a few options:

A high-yield savings account (HYSA) is a simple savings account. They are FDIC-insured and fully liquid.

Taxes: The interest on a HYSA is taxed at every level: federal, state, and local.

Marcus, Ally, and Capital One 360 are options I like (more about them here). As of writing, they are paying 3.1-3.6%. We’ll use the top of this range for comparison.

Their rates are variable and adjust fairly quickly as the general interest rate changes.

A Treasury money market fund is a brokerage fund holding very short-term US government debt. You buy these in your investment brokerage account just like you would any other mutual fund.

Taxes: Because Treasury funds hold government debt, the interest is exempt from state and local tax1. That’s very helpful if you live in a state or city with high taxes, but not helpful if you don’t.

A few things to keep in mind: The interest rates change with short-term rates and the interest is still fully taxable at the federal level. The fund is not FDIC-insured, though the risk is very low and balances held at a brokerage are SIPC-covered.

A municipal money market fund, (Muni), holds short-term debt from state and local governments. The rates also float and can be slightly more variable than other funds. They are not FDIC-insured but SIPC-covered.

Taxes: The interest is exempt from federal tax in all cases. And, if you buy your own state’s Muni fund (for example VCTXX in California) it is exempt from state tax as well.

Federal marginal tax rates are generally the highest part of your tax burden, so this is a valuable benefit when the tax savings make up for a lower interest rate.

Because there’s a few different tax savings options here and different starting interest rates we have to do a little bit of basic math to figure out which has the highest after-tax return in our case. That is what matters.

Vanguard’s Money Market Funds are consistently the highest return

Before we go on, a note about which brokerage offers the best funds. The answer is simpler than some of the other choices in this article. My clear favorite is Vanguard.

They charge lower fees than their major competitors, which allows them to pass on the highest return to you. For example, Vanguard’s Treasury Money Market Fund currently pays 0.3% more than Fidelity.

I’ll use Vanguard’s fund options in the rest of this article.

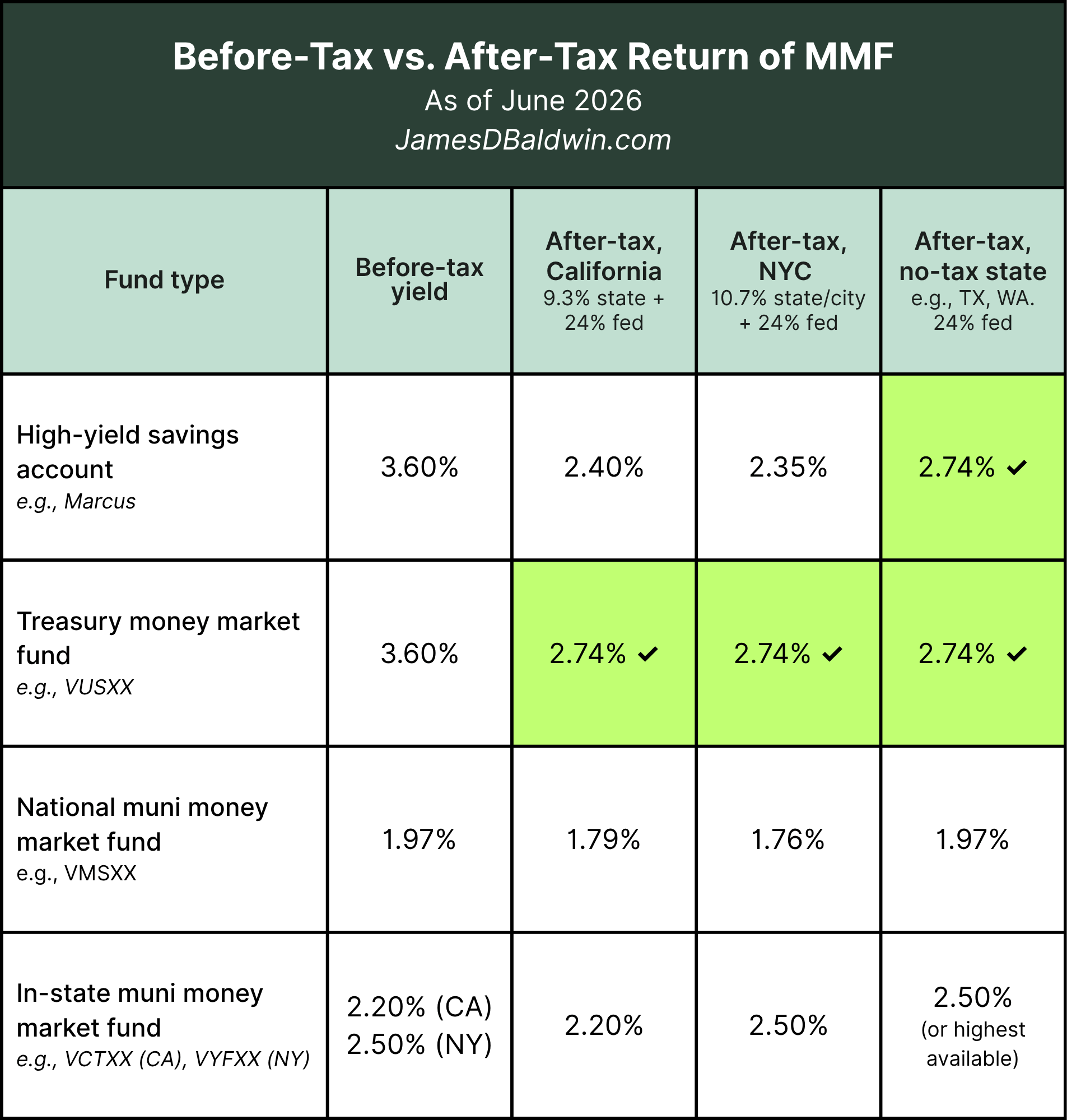

Before and after-tax yield, by fund type

Now let’s look at what after-tax return looks like in practice, as of today.

We’re going to use an example of a single filer earning $150,000 (married couples earning up to about $250,000 are in roughly the same position). We’ll use one example of a person paying taxes in California, one in NYC, and one in a no-tax state.

CA and NYC stand-in for high tax locations, but the actual after-tax rate will depend on your specific case.

At this income, the Treasury money market fund leads after-tax in all three locations with interest rates where they are today

In a high-tax state, the advantage comes from the state-tax exemption. In California:

The HYSA at 3.60% is taxed at every level. 3.60% × (1 − 0.24 − 0.093) = 2.40%.

The Treasury fund at 3.60% skips state tax entirely: 3.60% × (1 − 0.24) = 2.74%.

That means you’re earning 0.33% more than in a high yield savings account.

In a no-tax state, the state exemption stops mattering.

Both the HYSA and the Treasury fund are taxed at only 24% federal, so either one gives you the highest return.

The national muni fund carries a federal exemption but a low headline yield.

At a 24% federal bracket, the exemption saves 24 cents per dollar of interest.

But the starting yield is only 1.97%. Much lower than the Treasury fund. The tax saving does not overcome the lower starting interest rate.

The in-state muni fund (VCTXX in California, VYFXX in New York) is fully exempt from both federal and state tax, so the before-tax yield is exactly what you keep: 2.20% in California, 2.50% in New York. But this is again, not enough to make up for a lower starting interest rate.

This is the case for today’s interest rate and this specific tax rates. Unfortunately, it’s always going to be teh case that the Treasury fund gives the best after-tax interest rate.

The answer changes over time

The table above is a snapshot of June 2026. The absolute numbers will be different by the time you read this, and the relative rankings can shift too.

The gaps between instruments can change and at different speeds, which can change the conclusion. Right now, the national muni fund trails everything at a 24% bracket. At a different point in the rate cycle, or if you are at a higher bracket, that can change.

It’s worth rechecking once a year, or any time rates shift substantially.

What happens when you have even higher taxes

After-tax return depends on which taxes each fund avoids, which depends on how much tax you’re paying.

When your income increases and your marginal tax rate increases, that can change the conclusion.

A little-known tax for high earners: Net Investment Income Tax (NIIT)

Once your income passes $200,000 single or $250,000 married, a 3.8% Net Investment Income Tax (NIIT) applies to all invest income and interest, on top of your regular federal rate.

Because muni funds are exempt from federal tax, including NIIT, this can improve the relative after-tax return of muni funds.

Consider how this afftects a situation like a top-bracket Californian paying 37% federal, the 3.8% NIIT, and 12.3% state.

A California muni fund yielding 2.20% still returns 2.20% after tax because it avoids all taxes.

While a Treasury fund yielding 3.60% returns about 2.13%.

In this case, the fund with the lowest headline yield produces the highest take-home. The higher your federal rate, the more worth running the in-state muni comparison.

How to run your own numbers

The math is straightforward. Here’s how you calculate it:

After-tax yield = headline yield × (1 − your marginal rate on that interest)

The marginal rate is your federal bracket, plus 3.8% if you are over the NIIT threshold, plus your state and local rate, less whatever the instrument is exempt from.

A Treasury fund removes the state and local rate.

An in-state muni fund removes the federal rate and the state and local rate.

The high yield savings account is a reasonable choice when the balance is small and your taxes are low.

As the balance grows, the after-tax gap grows with it, and that is the point at which the MMF alternatives are worth a second look.

Of course, all of this assumes that you want to keep the money in cash so you can access it quickly. If you’re saving for longer time horizons, whether you want to keep it all in cash is not always obvious. I’m going to cover that tricky question in an article soon.

Want to learn more money strategies that matter for people earning $150,000+?

Some states, like California, require a Treasury fund to hold at least 50% in U.S. government obligations to qualify for the state tax exemption. Vanguard's Treasury fund typically meets this, but it's worth verifying annually.